2026 Fuel Crisis | What is the “Lion City’s” secret weapon in the fuel crisis?

Singapore’s fuel crisis does not primarily appear as empty petrol stations. It appears in prices, electricity bills, shipping, refining, regional demand, and in the question of whether a small city-state dependent on energy imports can keep both its domestic market and its role as an Asian energy intermediary functioning during a crisis. If Australia’s spring 2026 fuel shock became visible through long distances, diesel prices, and local supply disruptions, Singapore’s story is different: the country is vulnerable not only because it depends on imports, but also because others depend on it.

Singapore’s smallness is deceptive. On the map, it is a Southeast Asian city-state located between the Strait of Malacca and the South China Sea, with a population of just over 6 million people: 4.20 million residents and 1.91 million non-residents.1 But from the perspective of an energy crisis, Singapore is not simply a small island state. It is a port, a trading hub, an intermediary for petroleum products, and one of the world’s most important centres for marine fuel, or bunkering. This is where Singapore’s paradox lies: the country is vulnerable because it lacks a large domestic energy base, but strong because it has built itself into a hub through which fuel, goods, capital, and trust move.

Singapore’s protection does not come from independence in the classical sense, but from controlled interdependence: it depends on the world, but the world also depends on it — more than one might assume. This means that an energy crisis affects not only the domestic market or households, but the wider system through which goods, services, and capital move across the region. In Singapore’s case, the decisive question is therefore not only how much fuel the country itself consumes, but also how much the functioning of other countries, companies, and supply chains depends on Singapore’s reliability.

Major energy intermediary

Singapore’s role is best understood through energy flows. In 2024, the country imported 149 million tonnes of oil equivalent in energy products, 59% of which were petroleum products. At the same time, Singapore exported 78 million tonnes of oil equivalent in energy products, almost all of which were also petroleum products.² These figures capture Singapore’s specificity: it imports on a very large scale, but it is not merely an end consumer. Singapore processes, stores, trades, and redirects fuel to regional and global markets. At the same time, the country’s everyday functioning depends heavily on imported energy. This is illustrated by the fact that in 2024, 94% of Singapore’s electricity generation fuel mix came from natural gas.² As a result, a fuel crisis does not affect only cars, buses, or ships. It affects the entire technosphere of the city-state: from air-conditioning systems to hospitals and shopping centres, as well as the products and services that rely on them. If gas prices rise or supply becomes less certain, the pressure quickly reaches the ordinary functioning of the whole city.

Bunkering, or refuelling ships, is not a side service for Singapore; it is part of the country’s international role. Since most global trade moves by sea, it constantly needs fuel, insurance, maintenance, port services, and reliable logistics. Singapore’s strategic importance is especially visible in maritime activity, as shown by last year’s records: in 2025, the port reached a new high, with vessel arrival tonnage at 3.22 billion GT, container throughput at 44.66 million TEU, and almost 57 million tonnes of marine fuel sold to ships.³ These are figures of a scale that would give any maritime state confidence. This is also what makes Singapore’s crisis position difficult. The state must maintain domestic supply, keep the port and bunkering system functioning, and preserve its reputation as a reliable energy centre. If it restricts fuel exports too sharply, it damages its role as a regional hub. If its domestic buffer is too weak, pressure returns to the home market. The core of Singapore’s crisis management lies in this balance: protecting its own supply security without losing trust in its role as an international energy intermediary.

The Hormuz shock reaches Singapore through prices

Geographically, Singapore is far from the Strait of Hormuz, but in terms of energy flows it is much closer. In 2024, around one-fifth of global oil and petroleum product consumption and about one-fifth of global LNG trade passed through the Strait of Hormuz. For Singapore, the Asian dimension matters most: 84% of the crude oil and 83% of the LNG that moved through Hormuz went to Asian markets.⁴ This affects energy prices, shipping, insurance, refining, and electricity generation across the region. Even if Singapore’s port is operating and petrol stations have fuel, the shock still travels through prices. When crude oil, diesel, aviation fuel, or LNG become more expensive, the impact eventually reaches pump prices, electricity bills, transport costs, and the price of goods.

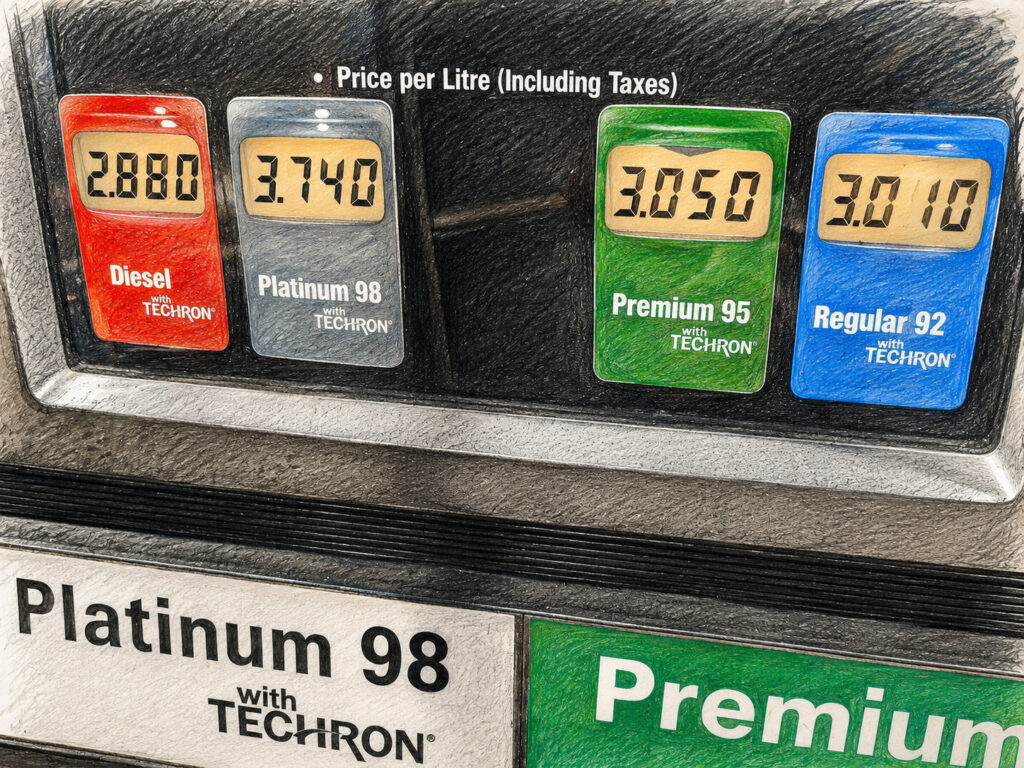

In spring 2026, this quickly became visible in Singapore. By late March, diesel prices had risen above S$4 per litre. On 30 March, Shell, Esso, and Caltex were selling diesel at S$4.13 per litre, SPC at S$3.92, and Sinopec at S$3.72. At the same time, 95-octane petrol remained at around S$3.40–S$3.42 per litre.⁵ The change was significant because, as recently as late February, diesel had been clearly cheaper than petrol at the major fuel retailers.⁶ Diesel price increases are central from a preparedness perspective. Petrol mainly affects private consumers and everyday car use, but diesel keeps goods, people, and services moving. In Singapore, this means buses, minibuses, vans, logistics companies, refrigerated goods, and a wide range of services.

The same price pressure also reaches electricity. Singapore depends on energy imports, and around 95% of its electricity is generated from imported natural gas.⁷ When oil and gas prices rise, the full impact does not appear immediately, because electricity and gas tariffs reflect earlier fuel costs. This makes energy crises deceptive: society may already be inside the crisis, while part of the cost pressure reaches consumers only later.

Protected, but not untouched

Singapore’s strength lies in the fact that its preparedness does not rest on a single solution. The country has diversified gas sources, fuel reserves, power plants that can switch to diesel, a strong port, energy trading capacity, refining capability, and diplomatic relationships. This does not make Singapore invulnerable, but it gives it more room for manoeuvre than a country dependent on a single terminal, pipeline, or supplier. Singapore cannot cut itself off from the global market. Its system reduces the risk of a sudden physical shortage, but it does not shield consumers from higher prices. This is especially visible in the electricity system. Natural gas reaches Singapore both through pipelines from Malaysia and Indonesia and as LNG from global markets. Power generation companies are required to maintain gas reserves and diesel reserves as an alternative fuel. If necessary, power plants can switch from natural gas to diesel and use the Standby LNG Facility.⁸

A contingency plan therefore does not only mean that there is a storage tank somewhere. It also means having the technical ability to switch the system. The same logic applies to national crisis management. Following the Middle East crisis, the Homefront Crisis Ministerial Committee was activated to coordinate the government’s response to energy, food, supply-chain, security, communication, and diplomatic risks.⁹ This matters because an energy crisis does not stay within the boundaries of one ministry. It touches foreign policy, ports, internal security, food supply, household coping, and public trust at the same time. In Singapore’s case, it is therefore necessary to distinguish between supply security and price security. The country has built a system in which a sudden physical shortage is less likely. But this does not mean that price increases will not reach consumers. Reserves, contracts, and diversified supplies help keep the system functioning, but they do not make a global crisis cheap. Preparedness does not make the world market cheaper. It helps avoid the worst.

Refining and bunkering as a layer of protection

Singapore’s protective layers are not limited to reserves. The country is the world’s third-largest oil trading centre and the sixth-largest exporter of refined products.⁹ This position is the result of deliberate industrial and trade policy. Refining gives Singapore a role that a purely consuming country does not have: it participates in the chain where crude oil becomes diesel, petrol, aviation fuel, marine fuel, and other chemical industry products. In a crisis, this gives Singapore access, weight, and information. The movement of large fuel volumes through Singapore means that the country is not at the edge of the market. Other countries’ need for Singapore’s refined products creates reciprocal relationships. Being at the centre of energy trading and port activity also gives Singapore early signals about where the market is moving.

The same capability also creates vulnerability. Refining requires feedstock, shipping, insurance, labour, electricity, and a functioning market. If crude oil, middle distillates, or semi-finished products become harder to obtain, a refinery cannot save itself on its own. If pressure on the Strait of Hormuz or other maritime chokepoints persists, it will eventually reach the refining hub as well. Singapore therefore cannot be only an intermediary or an observer in a crisis. It must seek alternative sources, maintain reserves, use diplomatic relationships, and ensure that domestic needs do not collide with international obligations. The same applies to bunkering. Readers often think of a fuel crisis through cars or petrol stations, but in Singapore’s case, it is also necessary to think about ships. When a container ship, tanker, or bulk carrier enters the Port of Singapore, it needs fuel to reach the next port. If fuel becomes more expensive or bunkering is disrupted, the impact quickly reaches logistics, insurance costs, and eventually the price of goods.

Singapore is protected by a balanced network

Singapore’s geopolitical position makes an energy crisis especially sensitive. The city-state cannot rely on one great power, one supply chain, or one political guarantee. Its economy needs open sea routes, rules-based trade, functioning relations with both the United States and China, strong ties with Australia and New Zealand, and a solid position within the ASEAN regional system. This is not neutrality in the sense of indifference, but deliberate balancing. Singapore cooperates with Western countries on defence and security, maintains economic relations with China, links itself closely to Australian and New Zealand supply chains, and seeks to preserve its role as a reliable, rules-abiding trading hub. In an energy crisis, this position becomes a practical layer of protection: when a country does not have large natural resources of its own, relationships, reputation, and agreements become part of supply security.

This is illustrated by Singapore’s relationship with Australia. One is a continental state and a major resource producer, but also a vulnerable importer of refined fuels. The other is a small city-state, but a major refining and trading hub whose electricity generation depends on imported gas. In a crisis, this relationship becomes a form of mutual energy insurance: Australia is an important LNG supplier for Singapore, while Singapore is a key source of refined fuels for Australia. This is not an ordinary seller-buyer relationship, but a mutual dependence between supply chains. It shows that fuel security is not only about what is located within a country’s own territory. It also depends on which relationships, agreements, and dependencies have been built before the crisis. When disruption comes, these links become practical: Australia can turn to a country with refining and trading capacity, while Singapore can rely on a politically close and reliable LNG supplier. The broader strategic partnership matters, but in a fuel crisis the question becomes very concrete: who can provide which critical resource to whom.

The same network also sets limits. Singapore cannot simply close the market during a crisis and keep everything for itself, because doing so would damage its credibility as a port, refining, and trading hub. At the same time, it cannot ignore domestic price pressure.

Singapore’s crisis management therefore depends on holding two levels together: the country must function internally while remaining reliable externally.

Lesson for Estonia: the state must know where its reserves will actually start working

Singapore’s example does not provide Estonia with a model to copy. Estonia cannot adopt Singapore’s strengths, such as refining capacity, the role of a bunkering hub, or a position in global energy trade. This is precisely why the lesson is sobering: if Estonia does not have the protective layer of a Singapore-type hub, it must know much more precisely what it can actually rely on in a crisis.

Reserves do not help enough if it is unclear how they will start moving during a crisis. The existence of fuel reserves is necessary, but it is not the same as functioning crisis capability. Reserves may exist in national accounting, but the practical questions in a crisis are different: how will fuel reach the places where it is actually needed, which sectors will receive it first, and how will this decision reach the petrol station network, companies, and local-level crisis managers? If these questions have not been thought through, a gap may emerge between official supply security and actual continuity of services. The state may have reserves, but a local service may still fail to access them in time. A municipality may have the task of opening an evacuation site, but no guaranteed access to generator fuel. Social transport may be listed in a crisis plan, but its contracted provider may not have assured refuelling access. In that case, the problem is not only the quantity of fuel, but the usability of the reserve.

This is where overly reassuring messages such as “crisis reserves exist” should be avoided. That may be true, but it does not yet answer how the reserve will work during a crisis. The public needs to know whether petrol stations will remain open, whether the state will restrict sales, whether critical services will receive priority access, and what ordinary people should do to avoid intensifying panic buying. Decision-makers need an equally clear situational picture: where commercial stocks are located, which petrol stations are critical, which regions are more vulnerable, and which transport corridors must remain operational. Without that information, crisis management quickly becomes guesswork.

“Fuel” must be broken down into concrete needs in crisis plans. The general word “fuel” can be deceptively convenient in a crisis plan. In reality, diesel, petrol, aviation fuel, generator fuel, and gas are not simply interchangeable. They keep different activities running and create different vulnerabilities. Diesel is critical for freight transport, agriculture, heavy machinery, waste management, generators, and many services that support continuity. Petrol is more closely linked to everyday mobility and some service providers. Aviation fuel is connected to connectivity and evacuation capacity. Generator fuel becomes critical when electricity supply is disrupted or when evacuation sites, communication points, care homes, or other critical facilities must remain operational.

For Estonia, this means that crisis plans should not merely ask stakeholders how much fuel they have stored. They need to ask more uncomfortable questions: what exactly is the fuel needed for; which services would fail first if, for example, diesel became harder to access; and which local government tasks depend on contractors who may not themselves have crisis-time refuelling rights? It also needs to be discussed which services are resilient on paper, but in practice depend on a single petrol station, a single carrier, or the assumption that the market will continue to function during a crisis.

If these questions are not addressed, responsibility can quickly shift downward in a crisis. The state may assume that municipalities will reorganise services locally. Municipalities may assume that service providers will find their own solutions. Service providers may assume that petrol stations will continue to operate. Residents may assume that the state will intervene before the situation affects them directly. This chain of assumptions may appear to work under normal conditions, but in a crisis it can reveal that each level has been relying on someone else’s capacity.

Estonia must also plan according to what it does not have. The most sobering lesson from Singapore is the need to recognise limits. In a crisis, Singapore can rely on its role as a hub for energy trading, refining, port services, and bunkering. Estonia does not have that position. This does not mean that international cooperation is unimportant. On the contrary, Estonia depends on it. But cooperation must not be treated as a vague sense of reassurance. It is necessary to distinguish between binding agreements, political promises, realistic supply channels, and wishful thinking. International belonging is necessary, but it does not replace a practical supply plan. In a crisis, concrete details matter: which ports are operating, which transport routes are usable, which companies can deliver, which fuel types are prioritised, which countries are competing for the same resources, and which agreements provide real access rather than general political support.

A fuel crisis cannot be treated only as a question of the size of reserves or international membership. It must be understood as a question of distribution capacity, local continuity, priorities, and responsibility. The most important thing is not to say that reserves exist. It is to know when, to whom, and how they become usable in practice. Domestic and regional layers of protection therefore become more important: clear prioritisation, rehearsed distribution decisions, a realistic role for municipalities, mapping the fuel needs of critical services, understanding the vulnerability of the petrol station network, and honest communication with residents. Small-state resilience does not begin with imagining the country as larger or more central than it is. It begins with knowing exactly when official assumptions no longer hold.

Photoe: Singapore fuel crisis illustrations (KRUK, 2026) and Singapore highrises (Pexels/Ethan Tran, 2023).

Sources

8 [Anon]., 2026b. How Singapore’s energy supply affects you. 10.04.2026, Energy Market Authority.

9 Shanmugam, K. 2026. Ministerial Statement on the impact of the Middle East situation on Singapore. 07.04.2026, Ministry of Home Affairs Singapore.

Jaga postitust: